Channel Saturation, Creative Architecture, & the Arbitrage Opportunity

A deep analysis of where HRIS advertisers spend, what they say, how their creative works and the structural white space a challenger can own. Based on ad library data covering 18,000+ active creatives across 7 channels and 5 competitors.

Why this report exists

Most HRIS companies are not losing because they lack budget, effort, or creative volume. They are losing because they are fighting the same battle in the same places, with the same messaging logic, against the same set of well-funded competitors.

This report exists to make that visible.

We wanted to move beyond surface-level ad spotting and show the deeper structure of the category: where HRIS advertisers actually spend, how concentrated their channel strategies have become, what kinds of creative narratives they rely on, and where the real white space still exists for a challenger willing to think differently.

The goal is simple: help revenue and demand leaders stop guessing. Not every opportunity in paid media comes from spending more. Some of the biggest wins come from recognizing where the market has become predictable, overpriced, and creatively interchangeable — and then moving where competitors are not.

That is the point of this report. To show where the category is crowded, where it is complacent, and where the next wave of efficient growth can still be won.

The biggest opportunity in HRIS advertising is not outspending competitors in crowded channels — it’s exploiting the channels and creative angles they keep ignoring.

Key findings at a glance

The clearest finding in this report is that the HRIS advertising market is highly active, but strategically concentrated. The biggest players — ADP, Rippling, Gusto, Deel, and Namely — are investing heavily in paid media, yet most of that spend is clustered into the same two channels: Google and LinkedIn. That creates the illusion of a highly diversified competitive market, when in reality it is a category built around a narrow set of acquisition habits. The result is predictable competition, rising costs, and diminishing differentiation in the channels where everyone is already present.

The second major finding is that the category’s creative strategy is far less mature than its media spend. Most advertisers over-index on bottom-funnel conversion tactics like demo requests, incentives, and feature-led calls to action, while underinvesting in identity, proof, and emotionally resonant problem framing. Deel stands out with a strong case-study and proof engine. Rippling stands out with narrative ambition and brand investment. Gusto stands out with SMB-friendly identity and full-funnel discipline. But across the category, one thing is almost entirely missing: vertical-specific creative that speaks directly to the real operating realities of SMB buyers.

That gap creates the biggest opportunity in the report. The next wave of winners in HRIS advertising likely will not come from spending more in defended channels, but from exploiting the white space competitors keep ignoring. Meta, YouTube, Reddit, and TikTok remain meaningfully under-owned relative to their cost efficiency and SMB buyer density. At the same time, no major player is pairing those channels with specificity-driven creative built for restaurants, field services, ecommerce, logistics, franchises, or other high-value SMB segments. The takeaway is simple: the opportunity is not to beat incumbents at their own game, but to attack the parts of the market they have left structurally exposed.

Channel Saturation & the Arbitrage Opportunity

The March 2026 HRIS paid media landscape is defined by a structural inefficiency. The category’s largest advertisers are highly visible, but narrowly concentrated. When we pull the full ad library data, the scale becomes clear: these five companies are collectively running more than 18,000 creatives across Meta, LinkedIn, and Google alone. But the vast majority of that inventory flows into the same two channels, aimed at the same professionalized buyer.

The result is not a lack of activity, but a lack of strategic dispersion.

Total Ad Library Footprint

Before examining channel-level strategy, the raw volume tells its own story:

The gap between the top of this table and the bottom is not a gap in budget alone. It is a gap in strategic ambition. Deel and Rippling are operating industrialized media systems. Gusto is running a disciplined acquisition engine. ADP is defending installed-base territory at scale. Namely is in maintenance mode. These are fundamentally different competitive postures, and the ad data makes them visible.

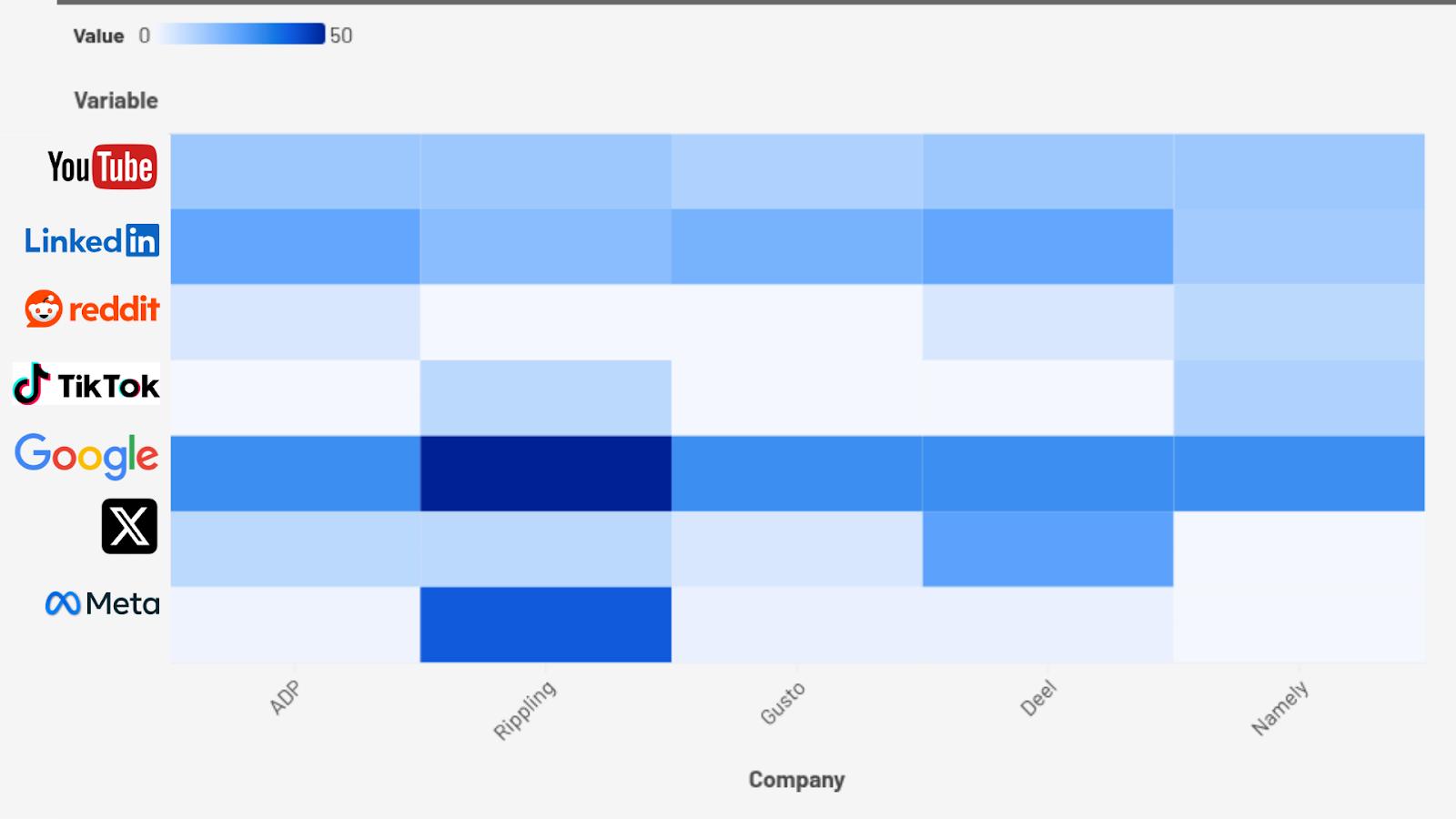

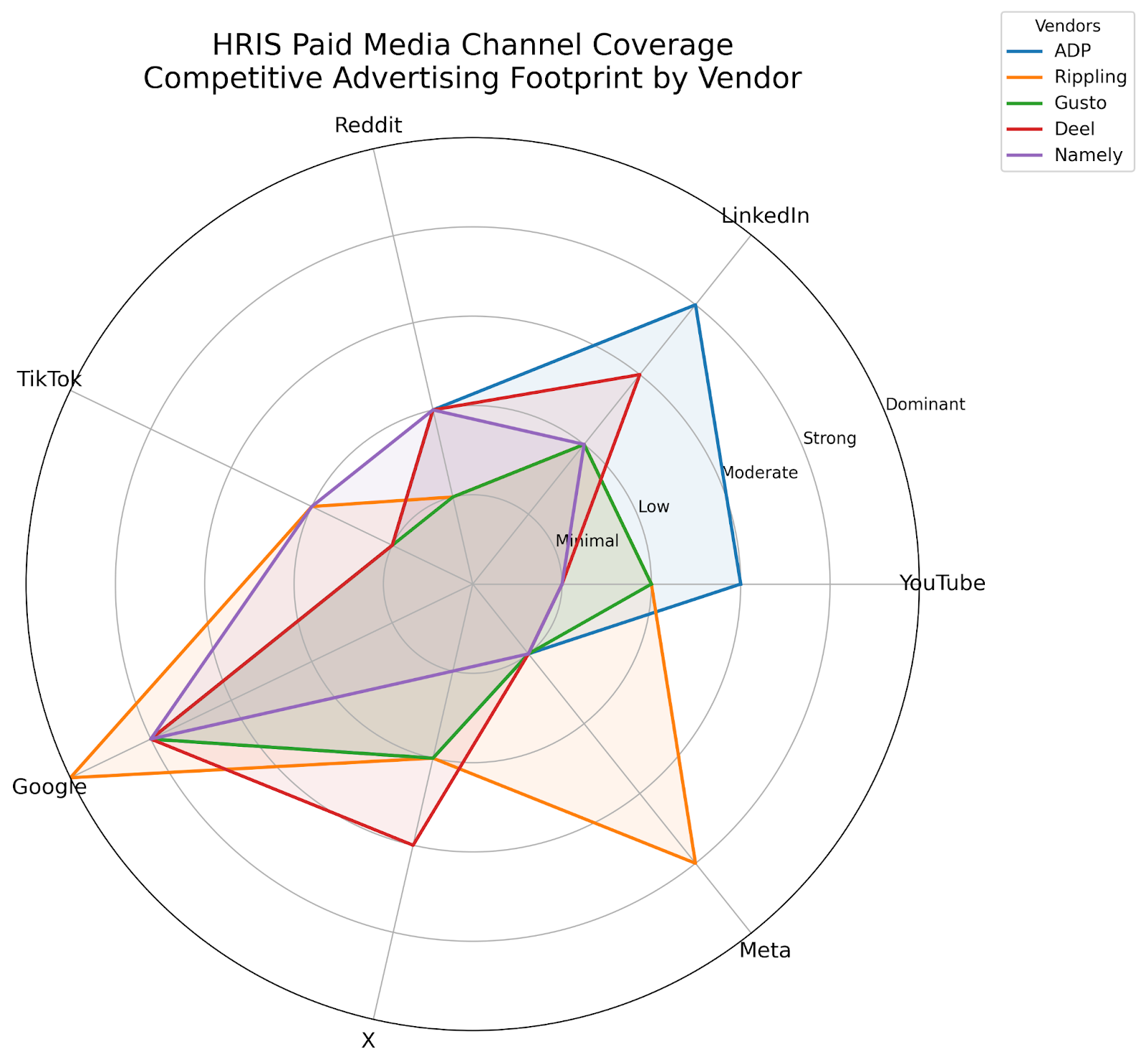

Active Channel Presence

While total ad library volume shows overall investment, active creative counts reveal where each company is currently visible in-market. LinkedIn and Google Search constitute the category floor — every vendor is present, making neither channel a source of differentiation.

Channel Concentration Heatmap

The heatmap (above) reveals the concentration pattern at a glance: Google and LinkedIn show consistent, deep blue across all five competitors. Everything else fades toward white — signaling sparse, inconsistent, or nonexistent presence. Rippling’s Meta activity is the lone exception to an otherwise homogeneous picture.

The coverage chart shows that this market is not experimenting broadly so much as clustering around the same few acquisition habits. Google is the one true constant across the set, while LinkedIn functions as the category’s default B2B amplification layer rather than a real point of differentiation. What stands out isn’t just where vendors are active, but how little separation exists outside those core channels, suggesting most players are competing in crowded, expensive environments while leaving newer or less saturated channels underdeveloped. Rippling appears to be the most willing to extend beyond the standard playbook, particularly with Meta, which makes its footprint look more intentionally diversified than the rest of the field.

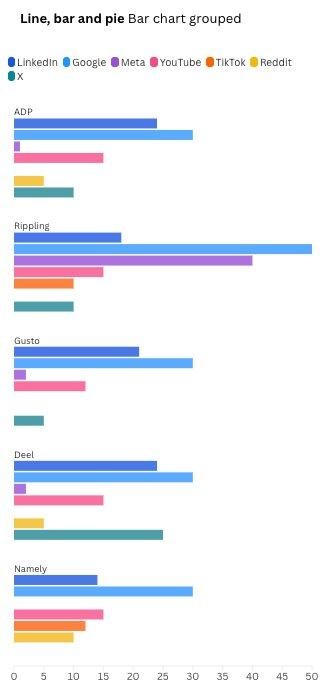

Creative Volume by Channel

Google and LinkedIn bars dominate for every company. Meta, TikTok, and Reddit barely register. This is a category that talks about omnichannel but operates as dual-channel.

Channel Saturation vs. Opportunity: The Math

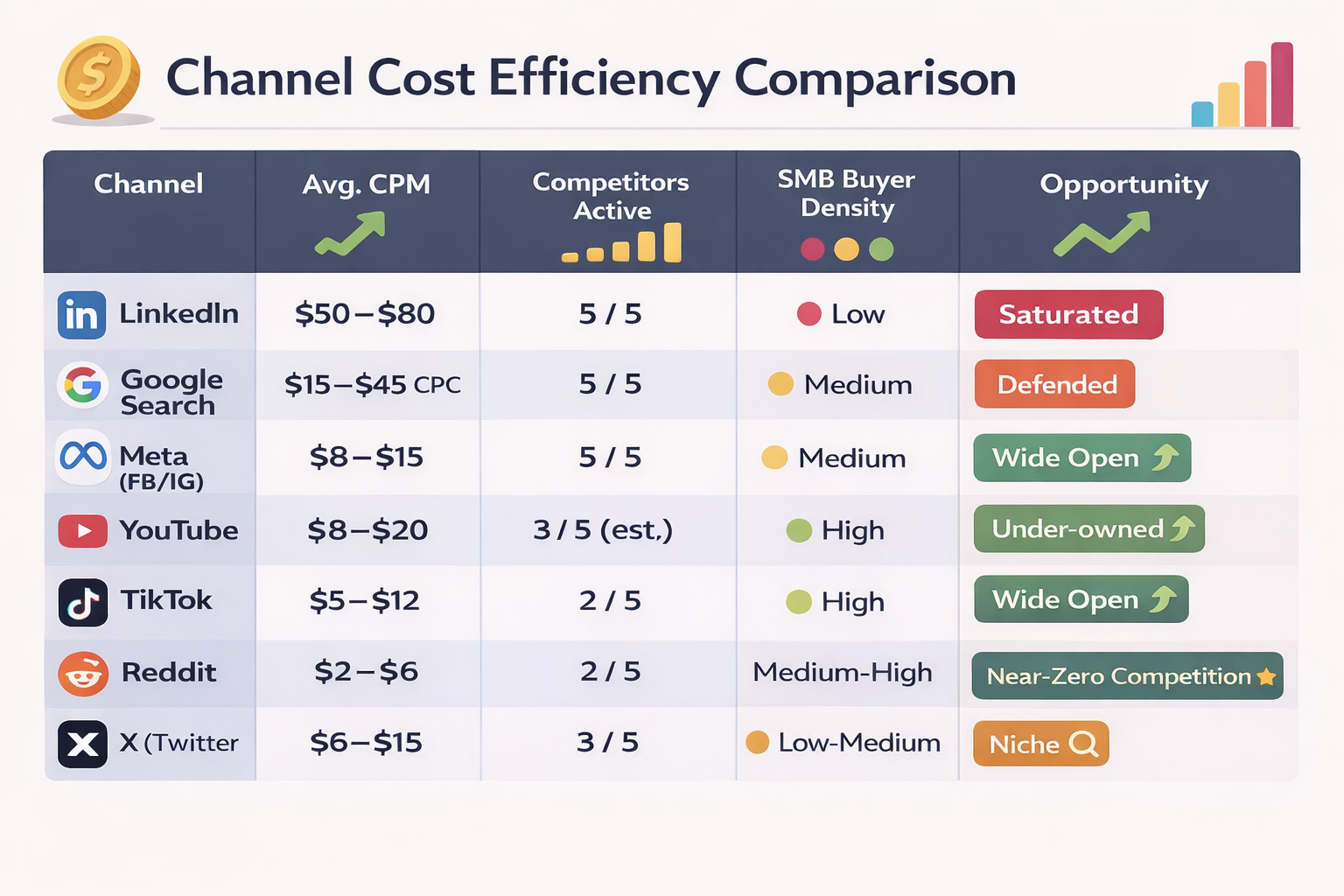

When we overlay competitive density against channel cost structure, the arbitrage becomes hard to ignore. LinkedIn remains the default buying environment for B2B marketers in HR and payroll, but that default comes at a steep premium. In the B2B HR category, LinkedIn CPMs commonly land in the $50–$80 range because every serious advertiser is chasing the same perceived professional audience in the same auction. Google Search is similarly defended: high-intent, yes, but crowded, expensive, and increasingly shaped by incumbents with larger budgets, stronger brand familiarity, and years of accumulated conversion data. For challengers, that means these channels often function less as sources of leverage and more as toll roads — necessary to some extent, but rarely where real cost-efficient advantage is created.

That matters because the actual economic buyer in much of HRIS is not always behaving like a polished “B2B audience segment.” For SMB payroll and people operations, the decision-maker is often the owner, operator, office manager, founder, or finance lead at a company with 5–50 employees — someone whose media behavior extends far beyond LinkedIn. That buyer spends time on Facebook and Instagram, watches YouTube to solve practical business problems, and often researches in communities like Reddit when they want candid advice rather than polished vendor messaging. In that context, Meta at $8–$15 CPM, Reddit at $2–$6, and YouTube pre-roll at $8–$20 are not just cheaper channels. They are places where buyer attention is both more affordable and, in many cases, more naturally aligned to the way SMB operators actually discover and evaluate solutions. The result is a 4–10x reach efficiency advantage before even accounting for the added benefit of lower competitive clutter.

That is where the arbitrage becomes strategic, not merely tactical. If incumbents are over-concentrated in LinkedIn and Search, challengers do not need to beat them head-to-head in the most expensive auctions to gain market share. They can build more efficient reach, create more repetitions per dollar, and sequence education across under-owned channels where competitors are either absent or underdeveloped. A dollar spent on Meta, Reddit, or YouTube does not just travel further — it often arrives in an environment with less direct category noise, giving creative more room to land. In practical terms, that means a challenger can fund a broader and more durable awareness-to-consideration system for the same budget that incumbents are using to buy expensive parity in crowded channels. The opportunity is not simply cheaper media. It is the ability to turn channel inefficiency in the category into strategic separation.

And the most important nuance is this: lower CPM alone is never the strategy. Cheap impressions are useless if they are disconnected from targeting, creative relevance, and measurement. But when low-cost channels are paired with vertical-specific messaging, CRM-connected audience segmentation, and stage-based creative sequencing, the economics become powerful. That is the real white space in HRIS advertising right now. The incumbents have largely optimized around channel habit. The next winner will likely optimize around channel mismatch — recognizing that the places incumbents undervalue are often the exact places where real SMB buyers can still be reached efficiently, repeatedly, and persuasively.

When we overlay competitive density against channel cost structure, the arbitrage becomes stark. LinkedIn CPMs in the B2B HR space typically run $50–$80. For owner-operators — the SMB buyers who actually make payroll decisions at companies with 5–50 employees — Meta can deliver equivalent reach at $8–$15 CPM, Reddit at $2–$6, and YouTube pre-roll at $8–$20.

That represents a 4–10x reach efficiency advantage against near-zero direct competition from incumbent HRIS advertisers.

The $8 Million Question: Rippling’s Super Bowl Bet

Nothing illustrates the channel allocation debate more vividly than Rippling’s Super Bowl LX debut on February 8, 2026. The 30-second spot — starring three-time Emmy Award-winning comedian Tim Robinson of I Think You Should Leave — cost approximately $8 million in airtime alone, before production, talent, and campaign integration.

Robinson plays a corporate villain in a spy-movie boardroom whose elaborate revenge scheme is comically derailed by mundane operational failures: a new hire hasn’t been onboarded, a laptop was never issued, finance has blocked a critical requisition. The tagline: “Don’t let bad software ruin your plans.” The five-ad series extends across streaming, social, and linear TV throughout 2026 as part of Rippling’s “Rule Your Business” campaign.

The creative execution was strong. But the channel math tells a different story about strategic allocation:

This is not an argument that the Super Bowl was a bad decision for Rippling. It signals ambition, and Rippling’s VP of Brand framed it as a deliberate shift from performance marketing to mass awareness — a legitimate move for a company with 30,000 customers and $1.8B in funding.

But it is a powerful illustration of the arbitrage: for the cost of 30 seconds of Super Bowl airtime, a challenger could fund an entire year of cross-channel paid media across Meta, YouTube, Reddit, and TikTok — with precision targeting, creative sequencing, and measurable pipeline attribution.

THE SIMPLE TAKEAWAY

Saturated channels: LinkedIn and Google Search.

Channel opportunities: Meta, YouTube, Reddit, and TikTok.

Creative Architecture & Competitive Messaging

Channel allocation tells you where competitors are visible. Creative architecture tells you what they’re actually saying — and more importantly, what they’re not saying. The analysis below draws on full ad library pulls across Meta, LinkedIn, and Google for all five competitors, providing a level of creative depth that goes well beyond active-creative snapshots.

The Four-Layer Messaging Framework

The entire category over-indexes at Layer 4 (Conversion) and under-indexes at Layer 1 (Identity) and Layer 3 (Proof). The result is a landscape of interchangeable demo requests with very little emotional or competitive differentiation — with two notable exceptions: Deel’s proof engine and Gusto’s brand identity.

Competitor Creative Deep Dives

Deel: The Category’s Most Operationally Mature Ad Machine

Deel is the benchmark for paid media maturity in this set: cross-channel, highly localized, proof-led, and relentlessly focused on business outcomes over product features. Their advertising suggests a company that has turned customer success stories into scalable demand infrastructure.

Deel’s ad footprint — 940 Meta ads, 7,539 LinkedIn ads, and 10,000 Google ads — makes it the most prolific advertiser in the set. But the more important signal is how that inventory is deployed. This is not random volume. It is a tightly repeated message architecture built around three ideas: global expansion without entity friction, compliance simplification, and proof-backed cost/time savings.

Across Meta, Google, and LinkedIn, Deel consistently avoids product-heavy jargon and instead sells outcomes: “cut costs,” “stay compliant,” “go global in days,” “centralize payroll.” That tells you they understand the market well enough to lead with business transformation, not feature checklists.

What makes Deel exceptional is its use of case studies as performance media, not passive website content. On Facebook especially, the ads are packed with named-customer proof and quantified outcomes:

- Directional Pizza: $74K saved in headcount costs and $100K+ in HRIS expenses

- Bitpanda: Onboarding cut from 3 months to 10 days

- Mynewsdesk: 120 hours of admin time eliminated

- BCG: Payroll centralized across six countries

- LMAX: International expansion without opening legal entities

Deel has turned social proof into a media system. These case studies are not sitting on a website waiting to be found — they are being actively distributed as ad assets, multiplied through dynamic creative optimization and headline variation across formats and geographies.

Another critical nuance: Deel is not running one global campaign with superficial translation. The same core offer shows up in English, French, Portuguese, and Spanish, with localized landing pages and regional framing. The ad operation mirrors the product story. Many HRIS vendors say “global.” Deel is one of the few actually behaving like a global operator in its media.

On LinkedIn, Deel combines standard product advertising with ecosystem-building: “The Pitch by Deel” (a founder funding competition), APAC breakfast events with J.P. Morgan, and employee-promoted thought leadership. This broadens reach beyond HR buyers into the startup and growth economy — creating brand adjacency with audiences that may become payroll, EOR, or HR platform buyers later.

Exploitable gap: Deel’s ICP skews heavily toward global, venture-backed, tech-forward companies. By targeting founders and international operators, Deel leaves the US domestic SMB payroll buyer almost entirely unaddressed. A challenger focused on “Payroll for American small businesses” with localized, vertical-specific creative can capture demand that Deel’s international narrative actively ignores.

Rippling: Category-Consolidation Machine

Rippling is not advertising like a point solution. They’re advertising like a category-consolidation machine — using ad volume not just for lead gen, but for market control.

With 6,932 LinkedIn ads, 830 Meta ads, and 3,000 Google ads, Rippling operates the second-largest ad footprint in the set. The sheer LinkedIn volume — nearly 7,000 ads — suggests broad persona coverage, heavy variant testing, persistent retargeting, and multiple product-line campaigns running simultaneously. This is a company trying to make Rippling feel inevitable.

Rippling’s creative operates on three simultaneous layers:

1. Category narrative creation. The “Software as a Disservice” and “State of Software Sprawl” campaigns don’t just advertise Rippling — they define the problem the market should care about. Fragmentation is the enemy. Disconnected tools are the villain. Rippling is the escape hatch. This is Challenger-brand positioning: teach the market that the status quo is broken, then own the fix.

2. The Super Bowl / Tim Robinson identity play. The “Rule Your Business” campaign starring Tim Robinson represents Rippling’s first serious Layer 1 (Identity) investment. Robinson’s villain-undone-by-bad-software character positions Rippling users as masterminds — smart, ambitious, in control. That’s a fundamentally different emotional register than “unify your people ops.” The five-ad series running across streaming, social, and linear TV throughout 2026 signals sustained brand narrative, not a one-off stunt.

3. Aggressive incentive-driven conversion. Rippling is very willing to use high-friction demo tactics: Apple Watches, Ninja CREAMis, SodaStreams, YETIs, Nike and Lululemon gift cards, and £100 Amazon vouchers all appear as demo incentives across LinkedIn and Meta. This likely inflates top-of-funnel demo rates while introducing significant quality risk — gift-card-motivated demos skew toward low-intent prospects who may not have genuine purchase urgency.

Exploitable gap: Rippling’s “all-in-one” promise is powerful but creates vulnerability. Not every buyer wants one giant system — some hear “unified platform” and think: hard migration, broad but shallow, operational lock-in. The heavy incentive strategy may juice demo volume but can create pipeline noise. And the zero Reddit presence, despite an otherwise aggressive posture, leaves community-based, research-phase buyers completely uncaptured. A precision challenger can win by being more exact, more verticalized, and more insight-driven.

ADP: The Incumbent Fortress

ADP is the market’s defensive heavyweight: everywhere, credible, and relentless — but often so broad that it leaves precision openings for sharper competitors.

ADP is not behaving like a challenger trying to win attention. It is behaving like an incumbent trying to make sure no buyer escapes the category gravity field. The footprint — 247 Meta ads, 4,822 LinkedIn ads, and 2,000 Google ads — is not a selective campaign strategy. It is a market-coverage strategy.

The messaging is disciplined and unsurprising. Across Meta, ADP leans into broad, durable themes: “Forward-thinking solutions,” “Be ready for any what if,” and “Work is constantly changing. ADP helps businesses change with it.” That language is intentionally non-specific. It is not trying to create a new buying frame. It is trying to reassure a very large market that the safest answer is still ADP.

There are really two ADPs showing up in the creative. The first is the enterprise-safe ADP: stability, scale, preparedness, operational maturity. The second is the SMB ADP: lighter, more personality-driven, with lines like “ADP knows small business.” ADP is segmenting by audience psychology, but not by a sharper problem narrative. Enterprise gets “trust us, we’ve seen this before.” SMB gets “let us handle it so you can do your thing.” Both are competent. Neither is disruptive.

The ADP Marketplace ads are strategically important. They reinforce platform breadth and ecosystem gravity — turning the pitch from “buy our tool” into “buy into our operating environment.” That’s a subtle moat signal for mid-market and enterprise buyers who want extensibility and lower switching friction.

Exploitable gap: ADP’s messaging is broad to the point of abstraction. It talks about change, readiness, and forward-thinking solutions, but says comparatively little about differentiated outcomes, vertical use cases, or sharp pain articulation. ADP is dominating presence, but presence is not the same thing as persuasion. A challenger does not need to outspend this machine. It needs to out-specify it. The winning counter-position is not “we also do payroll.” It is: better fit for a defined segment, faster time to value, stronger proof, clearer economics.

Gusto: The Full-Funnel Acquisition Engine

Gusto is not just competing in the category — it is trying to become the category’s default decision for small-business payroll.

Gusto does not look like a company running ads. It looks like a company operating a full-scale acquisition machine. With 422 Meta ads, 1,186 LinkedIn ads, and 2,000 Google ads, the footprint is not passive brand maintenance. It is an always-on, multi-channel growth system designed to create demand, capture intent, and convert at scale.

Despite the scale, the campaign architecture is not sprawling. On Meta, Gusto drives traffic to a tight set of landing pages — payroll, onboarding, tax savings, Gusto Solo — with repeated outcome-based headlines and direct-response CTAs. The messaging is remarkably consistent: payroll simplicity, unlimited runs, easy switching, small-business friendliness, support for solopreneurs, and trust signals like “400K businesses.” That repetition is not laziness. It is conviction. Gusto has identified the messages that convert and is scaling them ruthlessly.

On LinkedIn, Gusto mixes traditional product ads with two distinctive plays. First, the USA Luge sponsorship campaign provides emotional scaffolding: “Small business takes guts” and “Built for the bold” give payroll software borrowed energy, speed, and identity — things the category doesn’t naturally have. Second, creator-led founder content from people like Megan Lieu, Colin Rocker, and Will McTighe brings Gusto closer to the lived reality of independent workers and founders: loneliness, entrepreneurship, building a business after getting fired. These are identity stories, not feature stories. On LinkedIn, where audiences increasingly respond to personality-driven content, this is a strong strategic fit.

Gusto’s 79.96% direct traffic share — the highest in the set — proves the brand strategy is working. Buyers navigate directly to gusto.com rather than searching generic terms. That kind of brand pull is rare in HRIS.

Exploitable gap: Gusto’s scale makes it feel broad. The messaging is optimized for simple, widely-appealing SMB positioning, which leaves room for sharper vertical specificity: restaurants with tipped wages, logistics with seasonal hiring, ecommerce with 1099 contractors, franchise models, field-heavy labor. If everyone in-market has already seen “simple payroll” and “switch easily” ten times, the next wave of challengers creates separation by speaking to the pains Gusto flattens out. Reddit and community channels remain completely absent.

Namely: Still in the Conversation, No Longer Controlling It

Namely is still in-market, but it no longer feels like it owns its own fight.

Namely does not look like an active market aggressor. It looks like a brand in maintenance mode. The clearest signal is the channel footprint: zero active Meta ads, just 16 LinkedIn ads, and 62 Google ads — with Google running under Vensure Employer Services, not the Namely brand.

That distinction is important. Because this is not just a story about low volume. It is a story about diminished brand ownership. If Namely is not visibly owning search demand under its own name, the market is being taught to think about the solution through the parent entity, not the original product brand.

On LinkedIn, Namely is still present but lightly. The ads skew toward familiar HR-content themes: workplace challenges, compliance, hybrid work, lean teams, webinars, downloadable guides. The tone is helpful and serviceable but not especially urgent, differentiated, or forceful. This is classic nurture-layer creative — the kind you run when you want to stay credible with the audience, not when you’re trying to take share.

The absence on Meta is its own statement. In a market where other HCM players are using Meta for scaled reach, retargeting, and SMB acquisition, Namely’s complete absence suggests either channel de-prioritization, budget constraint, or a narrower belief about where the brand can still win.

Exploitable gap: Against Namely, the opportunity is not just stronger messaging. It is stronger conviction. A challenger wins here by sounding more certain, more specialized, and more alive. Where Namely sounds like a capable guide through HR complexity, a sharper rival sounds like the platform built for today’s operating reality. Where Namely offers practical resources, a rival offers a reason to switch.

Messaging Theme Matrix

The following matrix maps dominant messaging themes across competitors. The bottom row is the finding that matters most:

Messaging White Space

What This Means for Your HRIS Marketing

The data in this report points to a single conclusion: the opportunity is not to outspend incumbents. It is to exploit the category’s common blind spots.

Three Implications for Challengers

- The category is overspending in defended channels. LinkedIn and Search are modes of parity, not leverage. Rippling’s $8M Super Bowl bet is the most dramatic example, but the same logic applies to every competitor’s LinkedIn-heavy allocation. Even Deel — the most mature advertiser in the set — has built its media engine primarily around Google and LinkedIn, leaving Meta, Reddit, and TikTok for a challenger to own.

- Creative strategy lags channel reality. Deel has built the proof engine. Rippling has built the narrative engine. Gusto has built the brand engine. But nobody has built the vertical engine. Vertical-specific SMB creative is the largest category-level white space we have identified — and it is the creative approach most aligned with how owner-operators actually make buying decisions.

- Measurement maturity determines who wins. Only ADP and Rippling have full CRM-connected orchestration stacks. Deel has strong acquisition infrastructure. Gusto has disciplined funnel management. Namely has almost nothing. Whoever can connect signals (site behavior + CRM stage + persona + vertical) to creative sequencing will win the next 24 months of category spend.

About this report

Research & Report by Derek Rahn

This report combines primary ad-library data, market-cost benchmarks, and public campaign research to map how leading HRIS brands compete across paid channels. The analysis is grounded in large-scale creative pulls across seven major platforms, then layered with CPM/CPC benchmarks, public brand activity, and competitor context to interpret not just where companies advertise, but how they allocate spend, structure messaging, and expose strategic white space. The result is a category-level view of channel saturation, creative maturity, and the under-owned opportunities challengers can still exploit.