Y Combinator has always had a mythology problem. The outside world talks about YC companies as if they are all part of the same growth machine: elite founders, fast product iteration, venture capital, distribution hacks, and inevitable momentum.

But when you look at their active advertising footprint across Google, LinkedIn, and Meta, a very different story shows up.

Most YC companies are not advertising at meaningful scale. A small handful are absolutely flooding the market. And an even smaller group is doing the one thing that actually matters in modern go-to-market: turning paid channels into a real-time signal system.

Based on an April 2026 analysis of 5,906 YC companies run through LinkedIn, Meta, and Google ad data, the paid-media landscape is far more concentrated than most people would expect.

Across the file, the current ad footprint totals roughly 1.52 million ads, up from 1.02 million in September 2025. That is a net increase of 503,252 ads, or about 49% growth.

On the surface, that sounds like YC companies are leaning hard into paid acquisition. But the deeper truth is more interesting.

Of the 5,906 companies analyzed, only 2,013 companies had any active advertising footprint at all. That means roughly two-thirds of the YC universe had zero visible ads across the three major channels. Even among companies marked active, only 1,809 of 4,243 had any current paid footprint.

YC may be famous for growth, but paid distribution is not evenly distributed. It is a winner-take-most market.

The YC ad market is extremely concentrated

The most important finding is concentration.

The top 16 “super heavyweight” advertisers account for about 1.07 million ads, or roughly 70% of the entire advertising footprint in the dataset.

That is not a typo. Sixteen companies represent less than 1% of the advertisers in the file, but they control more than two-thirds of the visible paid-media surface area.

The top five alone — TypeLess, Lattice, Airbnb, Bizzy, and UserGems — account for nearly 58% of all tracked ad volume.

A paid-media footprint is not just a marketing metric. It is a GTM maturity signal. A company that suddenly increases visible ad activity may have new funding, a new growth mandate, a product launch, a category push, or board-level pressure to accelerate pipeline.

This is the part of the story that matters for revenue leaders: the startup market does not mature evenly. It stratifies. A few companies discover scalable distribution, build channel muscle, and start compounding. Everyone else is either experimenting, underfunded, product-led, reliant on founder/network-driven sales, or simply not showing up in paid channels.

The current paid-media leaders

The biggest visible advertisers in the YC file are not just the famous names. Yes, Airbnb, DoorDash, Stripe, Instacart, Deel, Rippling, Faire, and Segment all show up with meaningful footprints. But the most interesting names are the ones that are not obvious household brands.

| Company | Current ad count | Change vs. Sept. 2025 | Dominant channel |

|---|---|---|---|

| TypeLess | 304,334 | +304,334 | |

| Lattice | 201,424 | +74,228 | |

| Airbnb | 201,331 | -101,439 | |

| Bizzy | 141,181 | +141,181 | |

| UserGems | 33,885 | +9,482 | |

| Faire | 20,830 | +142 | |

| DoorDash | 20,603 | +10,078 | |

| Soomgo | 20,085 | -289 | |

| Podcast App | 20,000 | -10,000 | |

| Strikingly | 20,000 | 0 |

TypeLess is the single biggest advertiser in the file by current ad count, with more than 304,000 tracked ads and essentially all of that growth appearing since the September benchmark. Bizzy shows a similarly explosive jump, adding more than 141,000 ads and becoming one of the largest LinkedIn advertisers in the dataset.

That is the signal worth paying attention to. The YC companies worth watching are not always the ones with the loudest brand. They are the ones whose distribution footprint is suddenly expanding.

The momentum winners

If the current leaderboard tells us who has scale, the change column tells us who is pushing harder.

| Company | Current ad count | Net change |

|---|---|---|

| TypeLess | 304,334 | +304,334 |

| Bizzy | 141,181 | +141,181 |

| Lattice | 201,424 | +74,228 |

| Paribus | 11,938 | +10,762 |

| DoorDash | 20,603 | +10,078 |

| UserGems | 33,885 | +9,482 |

| Snappr | 7,037 | +7,002 |

| Photoroom | 7,399 | +6,320 |

| Cloudant | 4,214 | +4,214 |

| Medumo | 4,162 | +4,162 |

This is where ad data gets more valuable than a static company list.

A traditional database might tell you that a company exists, where it is headquartered, how many employees it has, and who works there. Useful, but incomplete.

A signal layer tells you who is moving.

When a company suddenly adds thousands or tens of thousands of ads, something has changed. It may have new funding, a new growth mandate, a new product push, a new market, a new demand gen leader, or a board-level pressure to accelerate pipeline.

The point is not that ad volume proves a company is winning. The point is that ad velocity reveals which companies are behaving like they are trying to win.

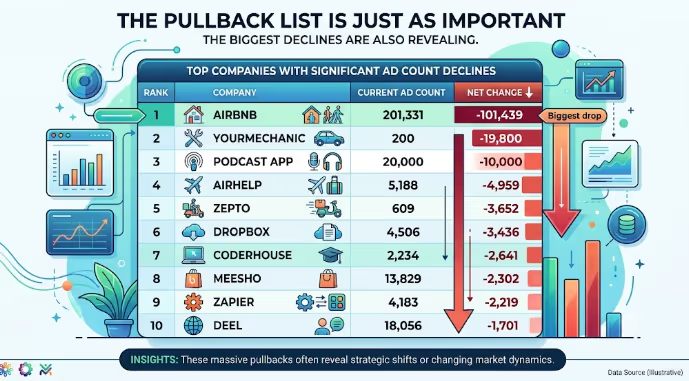

The pullback list is just as important

The biggest declines are also revealing.

| Company | Current ad count | Net change |

|---|---|---|

| Airbnb | 201,331 | -101,439 |

| YourMechanic | 200 | -19,800 |

| Podcast App | 20,000 | -10,000 |

| AirHelp | 5,188 | -4,959 |

| Zepto | 609 | -3,652 |

| Dropbox | 4,506 | -3,436 |

| Coderhouse | 2,234 | -2,641 |

| Meesho | 13,829 | -2,302 |

| Zapier | 4,183 | -2,219 |

| Deel | 18,056 | -1,701 |

This does not mean these companies are “losing” as businesses. Airbnb, Dropbox, Zapier, Deel, and Meesho are obviously meaningful companies.

But it does mean their visible ad posture changed.

Airbnb remains one of the largest advertisers in the entire YC universe, but it is also the largest absolute pullback in the file. Deel remains a diversified, mature paid-media operator, but its current count is down from the September benchmark.

Three kinds of losing

- Companies that appear to have stopped advertising because they are inactive, acquired, or no longer in growth mode.

- Companies that are still active but not visible in paid channels, which may indicate product-led growth, founder-led sales, capital discipline, or underdeveloped marketing infrastructure.

- Companies with meaningful prior ad footprints that are now pulling back, suggesting budget reallocation, channel fatigue, creative fatigue, market saturation, or a strategic pivot.

The mistake is treating all silence the same. A company with no ads may be disciplined. A company with collapsing ad volume may be correcting. A company with rising multi-channel activity may be entering a new GTM chapter.

Google owns the YC advertising surface area

Across the main company list, Google is the dominant channel by ad count:

Google is the biggest surface area because it captures intent. For many YC companies, especially consumer, marketplace, fintech, education, local services, travel, and high-intent B2B categories, Google is still the default performance channel.

The Google sample reinforces this. Of the 27,845 Google ad examples in the workbook, 71% were text ads, compared with 17% image and 12% video. The median duration between start and last-seen dates was 127 days, suggesting many campaigns are not just short tests. They are persistent acquisition plays.

LinkedIn, meanwhile, is the B2B proving ground. The LinkedIn sample includes 15,503 ad examples, and the format mix is heavily weighted toward sponsored status updates and image-based ads. Roughly 94% of the LinkedIn examples were image-based, with sponsored status updates representing the majority of creative types.

Meta is smaller in the dataset but still strategically important. The Meta sample includes 3,596 ads, and 96.6% were marked active. The most common call to action was “Learn More,” followed by “Shop Now,” “Sign Up,” and “Install Mobile App.” Meta appears less like the center of gravity for the full YC file and more like a channel for specific motions: consumer apps, ecommerce, mobile acquisition, marketplaces, and retargeting.

The real weakness: most companies are not multi-channel

The biggest strategic gap is not that companies are failing to advertise. It is that most advertisers are still channel-fragmented.

Only 169 companies in the file showed activity across LinkedIn, Meta, and Google. That is less than 3% of the full dataset.

| Channel footprint | Companies |

|---|---|

| No visible ads | 3,893 |

| LinkedIn + Google | 608 |

| LinkedIn only | 506 |

| Google only | 476 |

| LinkedIn + Meta + Google | 169 |

| Meta + Google | 135 |

| Meta only | 68 |

| LinkedIn + Meta | 51 |

This is the modern paid-media problem in miniature.

Most companies are either invisible, single-channel, or dual-channel. Very few have built a unified cross-channel acquisition system.

That matters because the buyer journey is not single-channel. A CFO might research on Google, see category content on LinkedIn, encounter retargeting on Meta, and then convert weeks later through branded search or a direct visit. If those audiences, messages, and exclusions are not coordinated, the company is not really running a GTM system. It is running a set of disconnected channel bets.

The average team does not have an ad platform problem. It has an audience coordination problem. The companies that win are the ones that turn first-party data, signal data, and channel activity into one connected operating system.

B2B is where the heat is

One of the clearest macro-patterns is the rise of B2B advertising.

B2B companies generated roughly 1.02 million ads, far more than any other company type in the file. They also accounted for the largest net increase, adding about 570,000 ads compared with September 2025.

Consumer companies, by contrast, generated about 354,000 ads but declined by more than 100,000 ads overall. That decline is heavily influenced by large pullbacks from major consumer names, especially Airbnb, but the pattern is still meaningful.

The YC advertising center of gravity has shifted toward B2B.

That is not surprising. B2B startups are under pressure to show pipeline, prove repeatability, and move beyond founder-led sales. The old YC playbook of “build something people want” is still necessary, but it is no longer sufficient. At some point, the best B2B companies have to build a demand engine.

Who is really winning?

The companies “winning” in this data are not simply the companies with the most ads. There are four types of winners.

1. The scale winners

These are companies with massive current visibility: TypeLess, Lattice, Airbnb, Bizzy, UserGems, Faire, DoorDash, Deel, Rippling, Stripe, Segment, and others. They have either built or inherited meaningful distribution engines. Their paid footprint is large enough that competitors, partners, and investors should pay attention.

2. The momentum winners

These are companies with large increases in advertising activity: TypeLess, Bizzy, Lattice, Paribus, DoorDash, UserGems, Snappr, Photoroom, Cloudant, and Medumo. These are the names that should trigger competitive monitoring.

3. The multi-channel operators

These are the companies that are not just buying ads but spreading activity across channels. Deel, Gusto, Guesty, Deepnote, Sunsama, and others show signs of broader channel orchestration. Multi-channel activity is a proxy for GTM maturity. It suggests a company is not just trying to capture demand. It is trying to create, retarget, convert, and measure it across surfaces.

4. The category heat winners

B2B, human resources, retail, recruiting/talent, infrastructure, engineering/product/design, finance/accounting, and analytics are all categories with meaningful paid footprints. The strongest category signal is HR tech. Human Resources companies represent only 85 companies in the file but generated more than 226,000 ads, driven heavily by large B2B players.

Who is losing?

The losers are harder to define, because a lack of paid ads does not automatically mean a company is weak.

Some YC companies do not need paid media. Some are too early. Some are developer-led. Some sell into narrow enterprise markets where ads are not the primary motion. Some are acquired or inactive. Some are intentionally capital-efficient.

But from a visibility standpoint, the companies losing the paid-media game fall into three buckets.

1. The invisible majority

The largest group is the 3,893 companies with no visible ads. Some may be healthy. Many are not. Either way, they are not competing for attention in the major paid channels tracked here.

2. The pullback group

Companies with large ad declines may be optimizing, cutting waste, shifting channels, or changing strategy. But they are worth watching because ad pullbacks often signal something operational: budget pressure, creative fatigue, channel saturation, new leadership, weaker CAC performance, or a pivot away from a prior growth motion.

3. The single-channel dependents

A company with one dominant paid channel may have focus. It may also have risk. If Google gets more expensive, LinkedIn performance drops, Meta targeting degrades, or creative burns out, single-channel dependency becomes a GTM liability.

The bigger lesson: advertising data is GTM intelligence

The point of this analysis is not to dunk on startups that do not advertise.

The point is that active advertising data reveals behavior that static company data misses.

A normal database tells you what a company is. Ad intelligence tells you what a company is doing.

That difference is everything.

When ad volume spikes, a market is moving. When a company expands across channels, the GTM motion is maturing. When a category’s ad footprint grows, competition is heating up. When a company pulls back, something changed.

This is exactly where the future of go-to-market data is headed.

The old model was static enrichment: company size, industry, location, title, email, phone number.

The new model is live signal intelligence: ad activity, hiring patterns, product launches, funding, new locations, technology changes, social traction, ecommerce motion, supply-chain changes, and buying-window indicators.

The best GTM teams will not win because they have the largest database. They will win because they know which accounts are changing before everyone else notices.

YC companies are often treated as a monolith. They are not.

Some are invisible. Some are experimenting. Some are scaling. A few are dominating attention. And a smaller few are building real cross-channel growth machines.

That is the real leaderboard. Not valuation. Not batch year. Not founder hype. The real leaderboard is who can turn market attention into a repeatable advantage.

Turn market movement into your next campaign list.

LeadGenius helps revenue teams build custom account and contact data around the signals that actually matter: ad activity, new product launches, location growth, hiring trends, ownership changes, funding, social traction, ecommerce behavior, onsite technology, and more.

Methodology note: This article uses the April 2026 YC advertising dataset provided by LeadGenius. Ad count is used as a proxy for visible paid-media pressure and creative surface area, not as a direct dollar-spend estimate. Platform API availability, ad-library visibility, geography, and sampling limitations may affect observed totals. Directional movement and relative concentration are the primary signals.