Why revenue leaders in fintech & banking use LeadGenius

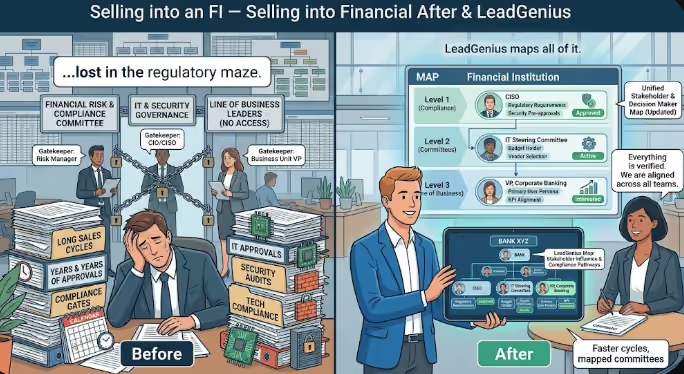

Selling into financial institutions means long cycles, heavy compliance gatekeepers, and committees that span risk, IT, and the line of business. LeadGenius maps all of it.

Nobody sells faster into a bank by knowing one more name. You sell faster by knowing the committee, risk, compliance, IT, and the line of business, before the cycle that is going to test all four even begins.

If you lead revenue at a fintech selling into financial institutions, a digital-banking platform like Bankjoy, an infrastructure provider like Plaid or Marqeta, or a spend platform like Brex, you sell into the most committee-heavy, compliance-bound buyers in the market. A bank or credit union decision pulls in a line-of-business owner, a head of digital, a risk officer, a compliance lead, IT security, and procurement. Every one of them can slow or stop a deal, and most of them never appear on a generic contact record.

That density is why fintech revenue leaders cannot run on off-the-shelf data. The buyer who champions you is rarely the buyer who clears compliance, who is rarely the buyer who signs. Reaching a financial institution means reaching a network of people, mapped correctly, before the long regulated cycle begins.

Compliance is a buyer, not a formality

In most software sales, security and compliance are a late-stage checkbox. In fintech and banking they are a buyer with veto power from the start. A risk officer or compliance lead can end a deal that the line of business loves, and frequently does. A seller who has not mapped and engaged that gatekeeper early is building a deal on a fault line.

LeadGenius builds the financial-institution committee with the risk, compliance, and security stakeholders included by design, mapped by responsibility across the inconsistent titles that banks and credit unions use. For a revenue leader, that means the deal is engineered around the gatekeepers from the first touch instead of colliding with them after months of work.

Trust and seller productivity are the fintech revenue fight

Long regulated cycles make seller time the scarcest resource in fintech. Every day an AE spends reconstructing who owns digital at a mid-size credit union is a day not spent advancing a deal that already takes the better part of a year. And when the leads marketing passes over are unverified, sales stops trusting them, and the funnel quietly breaks.

Those figures, drawn from enterprise GTM data programs, describe the fintech remedy exactly. Shifting seller time back to selling and lifting lead acceptance is not about volume; it is about verified, committee-complete accounts that an AE can actually work. In a category where each cycle is long and expensive, removing the research tax and ending the sales-marketing trust gap compounds across every deal.

Regulatory and institutional signals drive timing

Financial institutions move on triggers that flat data never shows: a new head of digital banking, a core-system migration, a funding round at a fintech, an expansion into new products or geographies that brings new compliance scope. Each is a window where a buyer has just acquired a reason to evaluate, and in a category with cycles this long, hitting that window early is decisive.

LeadGenius treats leadership changes, tech-stack migrations, funding, and expansion as research outputs, so a fintech revenue team can prioritize the institutions that just entered a buying window rather than working a static list. Reaching the new head of digital in week six instead of month nine can be the entire difference in a regulated deal.

The lower-lift second conversation

If your company has prior paperwork with an institution, the next conversation clears procurement and privacy review faster. LeadGenius surfaces those prior-relationship accounts so reactivation, not a cold compliance gauntlet, is the opening move.

Why another database does not close the gap

Fintech revenue leaders who have stacked databases know the limit. Risk and compliance officers are thinly and inconsistently covered everywhere, because they are not the contacts databases are built to surface. Buying a second source adds more line-of-business and marketing records and almost none of the gatekeepers a banking deal actually turns on.

LeadGenius is built for those exact targets. Because sourcing is a research brief, a fintech team can request the full committee, line of business, digital, risk, compliance, IT, at a named list of institutions, and receive data fit to a regulated sale rather than the generic intersection two databases happened to share.

Institutional data is wrong in ways that matter

Financial institutions are merging, rebranding, and reorganizing constantly, and generic databases lag all of it. A credit union that was acquired, a bank that spun up a new digital division, a head of digital who moved to a competitor, each is a data error that, in a regulated long-cycle sale, can waste months of an AE's time chasing a structure that no longer exists.

LeadGenius maintains institutional committees as a living deliverable, accounting for the consolidation and leadership churn that define the sector. For a fintech revenue leader, that accuracy is not cosmetic, in a cycle that already runs the better part of a year, starting from a correct map of the institution is what keeps the deal from stalling on bad assumptions.

What to ask for first

Run a committee-completeness benchmark on your top financial-institution targets, with explicit attention to whether the risk and compliance gatekeepers are mapped. Let LeadGenius show the gaps and the institutional signals you are not acting on. Revenue leaders in fintech and banking use LeadGenius because a regulated, committee-heavy sale is won by the team that maps the whole committee, gatekeepers included, first.

See the gaps in your own accounts

Ask for a complimentary coverage benchmark: hand us a slice of your target accounts and we will show where the committee is incomplete, where contacts have gone stale, and which accounts are showing live buying signals you are not acting on yet.

Connect with a strategistMore in this series

- Why revenue leaders in payment tech use LeadGenius

- Why revenue leaders in marketplaces use LeadGenius

- Why revenue leaders in cloud & SaaS use LeadGenius

- Why revenue leaders in HRIS & HR tech use LeadGenius

- Why revenue leaders in back-office software use LeadGenius

- Why revenue leaders in adtech & marketing tech use LeadGenius